How to Get Out of Debt Fast and Start Building Real Wealth (7-Step Proven Plan)

João and Rodrigo

12/9/2025

For millions, debt feels like a perpetual anchor, constantly pulling them away from their financial freedom. Whether it's high-interest credit card balances, student loans, or car payments, debt is the single biggest obstacle to building real wealth. You cannot truly grow your money until you stop paying crippling interest to others.

The good news is that the journey from being debt-ridden to building real wealth follows a clear, predictable path. It requires discipline, a powerful strategy, and a shift in mindset from spending to investing. This transition is not about waiting until you're rich; it’s about making proactive choices today.

In this comprehensive guide, we present a 7-step proven plan on how to get out of debt fast and, crucially, how to make the immediate shift into building real wealth. We will demystify the two most powerful repayment methods—the Debt Snowball and the Debt Avalanche—helping you choose the best route to secure your future.

Phase 1: The Debt Elimination Strategy (Steps 1-4)

The first phase focuses solely on minimizing interest payments and maximizing momentum.

Step 1: Stop the Bleeding and Build a Mini-Emergency Fund

Before you attack the debt, you must ensure you don't create new debt. The quickest way to derail your plan is an unexpected expense.

Stop the Bleeding: Cut up credit cards (while keeping the accounts open for credit score purposes) and commit to a cash-only approach for discretionary spending.

The Mini-Fund: Immediately save $1,000 in a separate, dedicated savings account. This acts as a buffer for small emergencies (e.g., flat tire, minor medical bill), preventing you from resorting to credit cards. This is a crucial foundation for building real wealth.

Step 2: List and Categorize All Debts

To get out of debt fast, you need total clarity on the enemy. Create a master list of every debt you owe, including:

Creditor Name

Total Balance Owed

Minimum Monthly Payment

Interest Rate (APR)

This list is the foundation for choosing your repayment strategy in Step 4.

Step 3: Slash Expenses and Find Extra Income

Your budget must become tight to free up "debt attacking" cash. Apply a strict budgeting strategy (like the 50/30/20 Rule: 50/30/20 Rule Explained: Budgeting Strategy for Smart Money Management) and find money to redirect.

Aggressive Cuts: Temporarily eliminate non-essential spending (Wants). Cancel unused subscriptions, stop eating out entirely, and minimize entertainment.

Boost Income: Dedicate your free time to earning extra money through a side hustle 10 Side Hustles You Can Start Today. Every dollar earned should go straight to the debt you are currently attacking.

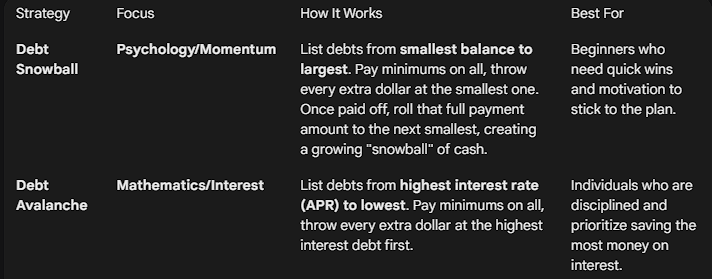

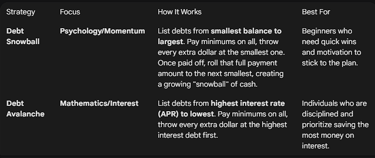

Step 4: Choose Your Debt Repayment Weapon: Snowball vs. Avalanche

This is the most critical decision in the plan on how to get out of debt. Both methods use the same money but prioritize different goals:

The Verdict: While the Avalanche saves the most money mathematically, the Snowball is often more effective because it builds psychological momentum, helping people stick with the plan long enough to truly get out of debt fast.

Phase 2: The Wealth Building Transition (Steps 5-7)

Once the high-interest debt (everything except your mortgage) is gone, you pivot immediately to building real wealth.

Step 5: Fully Fund Your Emergency Fund (The Ultimate Security)

Debt is gone! Now you can use the cash flow from your old debt payments to build a full emergency fund.

The Goal: 3 to 6 months of living expenses (rent, utilities, groceries) in a High-Yield Savings Account (HYSA).

The Why: This fund allows you to handle job loss, major medical events, or prolonged crises without ever having to borrow money again. This is the bedrock of financial freedom.

Step 6: Maximize Retirement Investing

With debt gone and the emergency fund in place, you must prioritize retirement savings, leveraging the power of time and compound interest.

The 15% Rule: Aim to save 15% of your gross income (before taxes) for retirement.

Employer Match: If your employer offers a 401(k) match, contribute at least enough to get the full match—that is 100% immediate, risk-free passive income: Passive Income Ideas for Beginners.

Roth IRA: For those just starting out, a Roth IRA is an excellent option, as withdrawals in retirement are tax-free.

Step 7: Invest Beyond Retirement and Achieve True Financial Freedom

With steps 1-6 complete, you are now in the elite group that is actively building real wealth. Your final goal is to generate enough passive income to cover your living expenses.

Beyond Retirement: Focus on brokerage accounts, real estate, or business ventures (like your blog!) to build wealth that can be accessed before traditional retirement age.

Invest in Knowledge: Your biggest asset is your ability to learn. Continue seeking knowledge about investing and wealth generation.

For highly detailed information on tax-advantaged accounts and retirement planning, refer to resources from a government body like the SEC (Securities and Exchange Commission).

💡 Your Freedom Starts Here

The transition from debt bondage to financial freedom is the most significant financial decision you will ever make. By committing to this 7-step proven plan, you are not just learning how to get out of debt fast; you are charting a course toward genuine financial security, where your money works for you, allowing you to finally start building real wealth.

Contact us

Reach out for questions or support

Phone

journeytomillion07@gmail.com

+55 11 98828-7504

© 2025. All rights reserved.